Should your credit rating are 750 plus, your odds of bringing home financing raise significantly, and even discuss to own all the way down interest levels for the loan providers.

- Realize Us

- Mouse click to express for the WhatsApp (Reveals in the the brand new window)

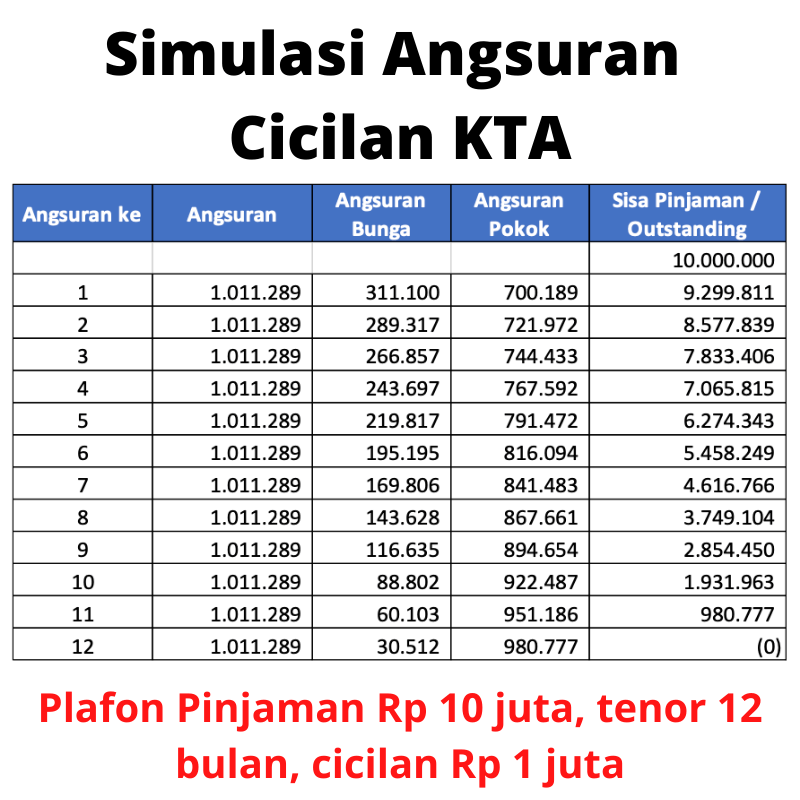

Financial rates is ascending, and you also should be wondering how to get the best income regardless of this persisted upsurge in repo pricing of the Set aside Bank out-of India (RBI). If you’re planning when deciding to take a mortgage and do not know how to check your qualification, then your first thing you ought to view is your credit score.

Credit score try a great three-hand matter between 300 and you will 900, determined by credit bureaus. A good credit score teaches you are designed for your debts better and you will pay-off her or him timely. You may want to avail worthwhile also provides towards the financial interest rates and you will handmade cards. When you first apply for a home loan, the financial usually ask you to answer about your earnings and look the credit score. Your credit rating is offered on your own credit history, and this summarises your past payments, non-payments, and mortgage debts.

Rising pricing? Score less than 7% interest lenders according to your credit rating

In case the credit rating is useful, you will get multiple advantages. One of the greatest advantages of which have a good credit score is that you can get a mortgage on a lower life expectancy interest. Continue reading “Ascending costs? Score less than seven% interest rate lenders based on your credit rating”